Supply Chains, Primary Products:

On this page

Summary

China macroeconomics

- China has set a growth target of 5% for 2023. This is modest compared to China’s pre-pandemic targets, and many analysts were initially bullish that China would easily surpass this target following China’s reopening in early 2023 after almost three years of COVID-related restrictions.

- China’s official data showed that China’s economy initially rebounded quickly following reopening, posting 4.5% year-on-year (and 2.2 % quarter-on-quarter) GDP growth in quarter one (Q1) 2023. Pent-up consumer demand drove growth in household consumption, services (particularly domestic travel), and increased property sales (from a low base). China’s export growth in Q1 2023 surpassed market expectations expanding by 14.8%.

- The growth momentum did not however carry through to quarter two (Q2) 2023. While China’s economy expanded by 6.3% yoy (0.8% GDP growth quarter-on-quarter), the result reflected the low comparison base in 2022 and missed market expectations (of 7.3%). Consumer demand stalled, export demand declined, and other economic indicators also softened over April-June. Economic commentators now agree that China’s economic recovery has lost its initial post-pandemic momentum.

- Risks in China’s macroeconomic environment remain: property market recovery has stalled; significant local government debt; and record high youth unemployment at 21.3%. Consumer inflation flattened in June and dropped in July; deflation shows consumer demand remains weak and is not an incentive for consumption.

- With tepid economic data, China’s central bank has cut its main benchmark lending rates to stimulate household and the private sector borrowing. On July 19, China’s State Council announced “31 policy principles” to support the growth of the private sector and improve the business environment. Economists interpret these moves positively, but contend more demand-side stimulus is needed.

Aotearoa New Zealand-China trade

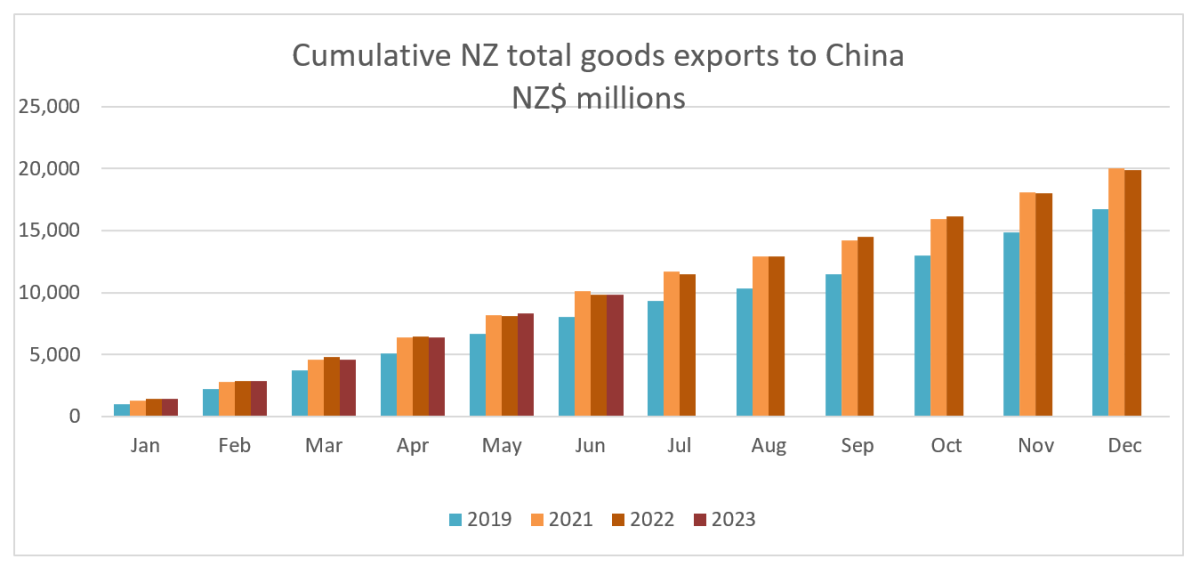

- China was Aotearoa New Zealand’s top trading partner in the year ending December 2022, with two-way goods and services trade totalling NZ$40.32 billion. Total exports of infant formula, fruit and meat products increased on 2021 levels.

- Cumulative goods exports in June 2023 totalled NZ$9.8 billion, on par with 2021 and 2022. Services exports in Q1 2023 have grown compared to 2021 and 2022 figures (NZ $560K), but still lagged pre-pandemic numbers by some margin (2019 Q1 NZ$1 billion).

- Air connectivity between China and Aotearoa New Zealand continues to improve with the reinstatement of air services. Current air connectivity has recovered to over half of 2019 summer peak season levels.

Report

Quarter one: sound start to economic recovery

The removal of Zero-COVID restrictions saw China’s economic activity normalising in early 2023, with 4.5% GDP growth year-on-year in Q1 2023, up from a low base of 2.9% in Q4 2022. Services spending drove economic growth, particularly in the domestic travel and hospitality sectors. Retail sales growth was 18.2% for Q1 2023 yoy. Household consumption improved from a low base in Q4 2022, but has yet to return to pre-pandemic levels. Exports performed strongly in Q1 2023, with particularly solid demand from emerging markets. During January to March the property sector had its first growth in sales in over a year.

Thriving domestic tourism

Domestic travel has been a standout since the removal of COVID restrictions. During the Labour Day holiday in early May, 274 million domestic tourist trips were made, a 71% increase on 2022 and 19% higher than the pre-pandemic year of 2019. Spending was however only 1% higher than in 2019.

China’s spending on international tourism remains low, with international passenger numbers in March 2023 only 20% of March 2019. While bookings are increasing and loadings to New Zealand are at respectable levels, Chinese tourists remain generally cautious about overseas travel.

Strong export growth

China’s Q1 2023 export growth surpassed market expectations expanding by 14.8%. The strongest performers were solar cells and electric vehicles, up 53.2% and 58% yoy respectively.

In April, China surpassed Japan to become the world’s largest exporter of automobiles. This was due to the rapid export growth of China’s EV producers (including BAIC, and Build Your Dream (BYD) brands) and growth in foreign auto manufacturers exporting from China (e.g. including from Tesla’s Shanghai expanded gigafactory with its claimed capacity of up to 1.25 million vehicles a year). Chinese government customs statistics showed China exported 1.07 million vehicles in Q1 2023, up 58% compared to the first quarter of 2022. First quarter exports of new energy vehicles (NEVs), which includes electric cars, rose by more than 90% yoy.

Quarter two: a slowing of momentum

Market expectations missed

Official economic data showed China’s economy continued to expand in Q2 2023 but the growth rate slowed, with GDP up 6.3% yoy, and 0.8% quarter-on-quarter. However, the high yoy result comes off a low base in 2022 (when Shanghai was in a two-month hard lockdown) and it missed general market forecasts of 7.1% GDP growth. Other economic indicators also slowed: retail sales fell by 12.7% yoy in May, and grew only modestly by 3.1% in June yoy; catering sales and credit growth softened in both April and May; manufacturing activity contracted during April to June, off a higher February base; new property sales dropped; property investment contracted; manufacturing activity slowed; and private firm investment only registered a slight increase.

China in Q2 2023 still had some strongly performing sectors: in May, the manufacturing output of solar cells, new-energy vehicles and service robots went up by 53.1%, 43.6% and 34.3% yoy respectively. Services activity grew over the April-June period. Private sector credit growth remained stable at 9.2%. With weaker-than-expected economic indicators, commentators warned the economic recovery remained uneven and was weakening.

Consumer deflation and declining export growth: weak consumer demand at home and abroad.

Official inflation data showed that China edged into deflation. Consumer prices were flat yoy in June and declined 0.2% compared with the previous month, while factory gate prices fell at the fastest pace since 2016. In July consumer prices dropped by 0.3% yoy, the first decline since February2021. Analysts suggested the falling prices underscored weakening domestic consumer demand and the dissipation of demand arising from reopening from Zero-COVID.

Declines in export demand has also contributed to deflation. China’s export growth contracted 12.4% yoy in June and again by 14.5% yoy in July, dropping for a fourth consecutive month. China’s General Administration of Customs attributed the steep decline to a global inflationary environment and tense geopolitics dampening demand for Chinese exports. Exports to Southeast Asia dropped 16.9% yoy in June and 21.4% yoy in July, compared to a 7.2% yoy increase in the first five months of the year, showing demand also softening in markets less-impacted by inflation.

An emerging concern is the drop in imports. Imports fell by 12.4% yoy in July, compared to a 6.8% yoy decrease in June. Analysts have categorised the drop in imports as another signal of weakening consumer demand.

Government’s strong economic narrative

2023 Growth target: 5%

At the Chinese National Party Congress in March, outgoing Premier Li Keqiang announced China’s annual GDP growth target: 5% for 2023. Set against the economic disruptions of 2022, analysts were bullish on China’s economic prospects for 2023 and viewed the 5% target as relatively modest. However, weak economic data in recent months has seen a number of major banks revise down their growth forecasts from >6% to closer to 5%.

In June, newly appointed Premier Li Qiang used his second major public speech, at the World Economic Forum’s ‘Summer Davos’, to express confidence in China attaining the 5% growth target. Speaking on the country’s economic trajectory, Li said China would promote development while accelerating the green transition and further opening up "high level" parts of its economy to the outside world.

Macroeconomic challenges remain

Falling national unemployment; but youth unemployment reaches record high

China’s overall national unemployment rate has been declining, and is now 5.2% from a high of 6.1% in April 2022. However, there are concerns about record high youth unemployment, which climbed to 21.3% in June. This number will likely increase further as more university students graduate in July.

Property sector slump

The property sector continues to be a drag on the China’s economic recovery. The Economist Intelligence Unit estimates that 70%of China’s household wealth is tied up in real estate. After a strong start in January and February, official data shows property sales cooled from April onwards, and new home sales growth has slowed to –18%. In the first half of 2023, new construction starts fell by 24.3% yoy. Housing prices have been slipping in smaller cities, and that decline spread to some big cities in June. National Bureau of Statistics on Saturday showed that its 70-city index of housing prices falling at an annual rate of 2.2 percent in June, after eroding at an annual rate of only 0.2 percent in May.

Local government debt

Significant local government debt and the risk of a credit blowout continues to hang over the economy. The total debt of China's Local Government Financing Vehicle (LGFVs) – a key financial mechanism to fund infrastructure – has increased to a record 66 trillion yuan (US$9.2 trillion), equivalent to half of the country's economy, from 57 trillion yuan last year, according to the International Monetary Fund. With a slow property market reducing local government income from land sales, and few other options for raising funds, local governments’ are focused on debt repayments and cutting discretionary expenditure. The ability of fiscally stretched local governments to undertake spending to support growth, while meeting debt obligations, will be a key hurdle for achieving China's 2023 GDP growth target.

Rate cuts and calls for more policy support

The softening of economic indicators and toughening international environment has commentators calling for policy support to stimulate the economy, in response there have been notable pivots in China’s monetary policy. In June, China’s central bank started modest monetary easing, cutting its main benchmark lending rates: the medium-term lending rate from 2.75% to 2.65%; one-year loan prime rate from 3.65% to 3.55%; and the five-year rate by the same margin to 4.2%. These actions look to stimulate households and the private sector’s borrowing and investment amid weak market sentiment. Commentators view the rate cuts as a ‘good start’ but stress further policy support is likely required for a sustainable economic recovery.

In the property sector, supportive policies already exist. Record low interest rates for new mortgages and the relaxation of home purchasing restrictions in many cities create a favourable environment for homebuyers. Further policy support, in the form of lower interest rates or easing mortgage lending restrictions, will probably be implemented to stimulate demand.

Analysts are less hopeful that sector non-specific demand-side policy support will be implemented. Some local government have implemented modest cash handouts or voucher programmes but these are sporadic and analysts doubt this will be replicated at a national level. Market watchers have described the current approach as “hands off”. The People’s Bank of China statement on 14 July said recent growth challenges were a “natural phenomenon of the post-pandemic economic recovery process.”

Government signals focus on private sector development

Following the release of disappointing Q2 2023 economic data on 17 July, China’s State Council announced “31 policy principles” to support the growth of the private sector. The principles fall into seven broad categories:

- optimising the development environment for the private sector

- increasing policy support for the private economy

- strengthening the legal protection for the development of the private economy

- promoting high-quality development of the private economy

- foster the healthy growth and development of private entrepreneurs

- creating a sustained social atmosphere that supports and promotes the growth of the private economy

- ensuring implementation of relevant policies

On 24 July, at the Politburo’s quarterly meeting on the economy, China’s leadership acknowledged that weak demand was a problem. President Xi stated the economy was: “facing new difficulties and challenges, mainly insufficient domestic demand.” Despite this, no major policy changes were announced at the Politburo meeting. While analysts have interpreted this shift in tone as a positive signal, the lack of specific measures for implementation suggests the government will continue to show restraint on economic stimulus.

Aotearoa New Zealand China trade

Improving Air Connectivity between Aotearoa New Zealand and China

Prior to the COVID-19 pandemic, five Chinese airlines and Air New Zealand operated services between China and Aotearoa New Zealand, amounting to up to 49 flights operating between the two countries weekly during summer peak season. As China Southern, China Eastern and Air New Zealand operated reduced services throughout the pandemic, these airlines were able to quickly ramp up weekly frequency of fights following the progressive lifting of China’s border restrictions from January 2023.

Throughout the pandemic Air New Zealand operated one passenger flight between Auckland and Shanghai per week. This increased to three in January, four in February, and is now daily. In April/May, Air New Zealand launched intermodal upstream check-in services in Guangdong, enabling passengers to check-in at ferry ports in Guangzhou and Shenzhen for its service from Hong Kong International Airport.

Summary of reinstated air services by Chinese airlines in 2023:

- In February, China Southern, China’s largest airline, increased the frequency of flights on its Guangzhou to Auckland route from twice to four times weekly, and in April it resumed daily flights. In June, during Prime Minister Hipkins’ visit to China, China Southern announced the resumption of the Guangzhou-Christchurch route with three flights a week and three additional services between Guangzhou and Auckland, both starting from November.

- In early May, Air China resumed its service between Beijing and Auckland, suspended at the start of the COVID pandemic. This service now operates four times per week, consistent with off-season frequency pre-pandemic.

- China Eastern resumed daily flights from Shanghai Pudong International Airport to Auckland from 27 March.

- Privately owned Hainan Airlines started selling seats on its service between Shenzhen and Auckland, and resumed 17 June.

- Sichuan Airlines is the only Chinese airline that serviced Aotearoa New Zealand (Chengdu-Auckland) pre-pandemic, that has not announced plans to resume its service to New Zealand.

Current flight capacity:

- Air New Zealand – 7 x per week (Shanghai)

- Air China – 4 x per week (Beijing)

- China Eastern Airlines – 7 x per week (Shanghai)

- China Southern Airlines – 7 x per week (Guangzhou)

- Hainan Airlines – 2 x per week (Shenzhen)

- Total: 27 flights per week

Aotearoa New Zealand exports to China

China was Aotearoa New Zealand’s top trading partner in 2022, with two-way goods and services trade totalling NZ$40.32 billion. Over this period China remained Aotearoa New Zealand’s largest market for total exports (NZ$21.37 billion) and imports (NZ$18.95 billion), despite the continuing challenges for services exporters.

For goods exports in 2022, China was Aotearoa New Zealand’s largest market (NZ$19.9 billion), a slight (0.7%) decrease on 2021.

Goods exports have been steady over the first six months of 2023, reaching NZ$9.85 billion by 30 June, a 0.5% increase over the first six months of 2022. The following section of the report looks at key export products in more depth.

Total goods exports

Dairy (not including infant formula)

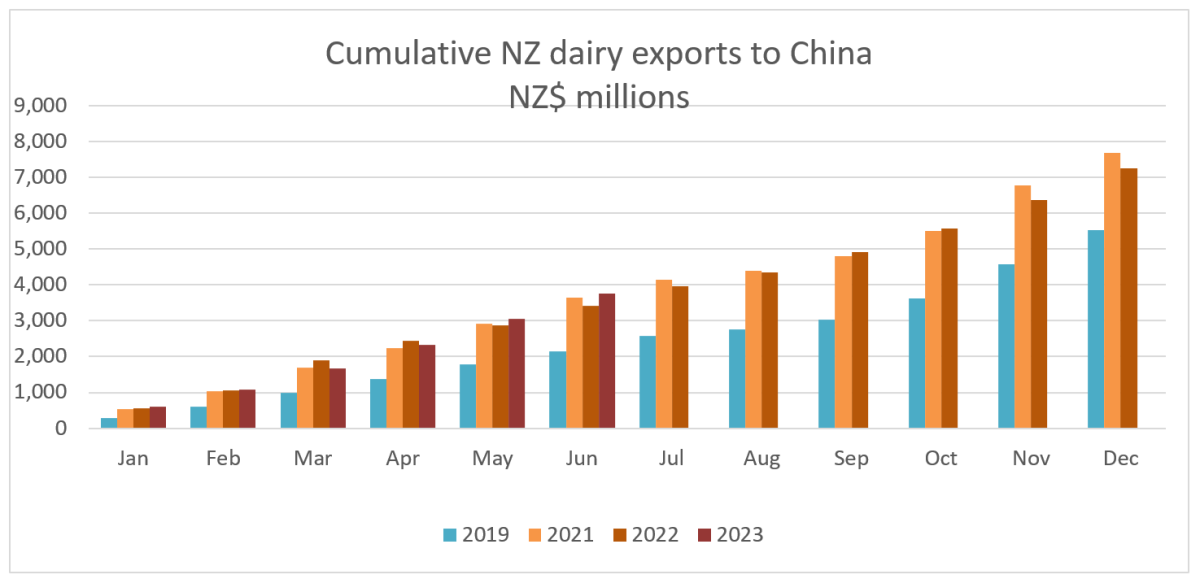

Aotearoa New Zealand’s dairy exports to China in the year ending December 2022 totalled NZ$7.2 billion, down 5% on 2021. However, in the six months to June 2023, export value has rebounded, growing almost 10% yoy. Pandemic demand for dairy products largely held up despite lockdowns impacting consumers. 2022 saw some weaker consumer demand for both domestic and international dairy products and China’s stockpile of dairy product grew ahead of actual demand from consumers. The Chinese government has been pushing for consumers to increase dairy consumption (e.g. through health and science education and promotion). China’s domestic dairy industry has continued to grow its national herd, improving supply chain links, and increasing feed supply. These measures may have contributed to the growth in dairy export returns in 2023, though a higher value product mix may also be a factor. Greater Chinese and global supply availability of dairy may put some put downward pressures on prices in Q3 2023.

Infant Formula

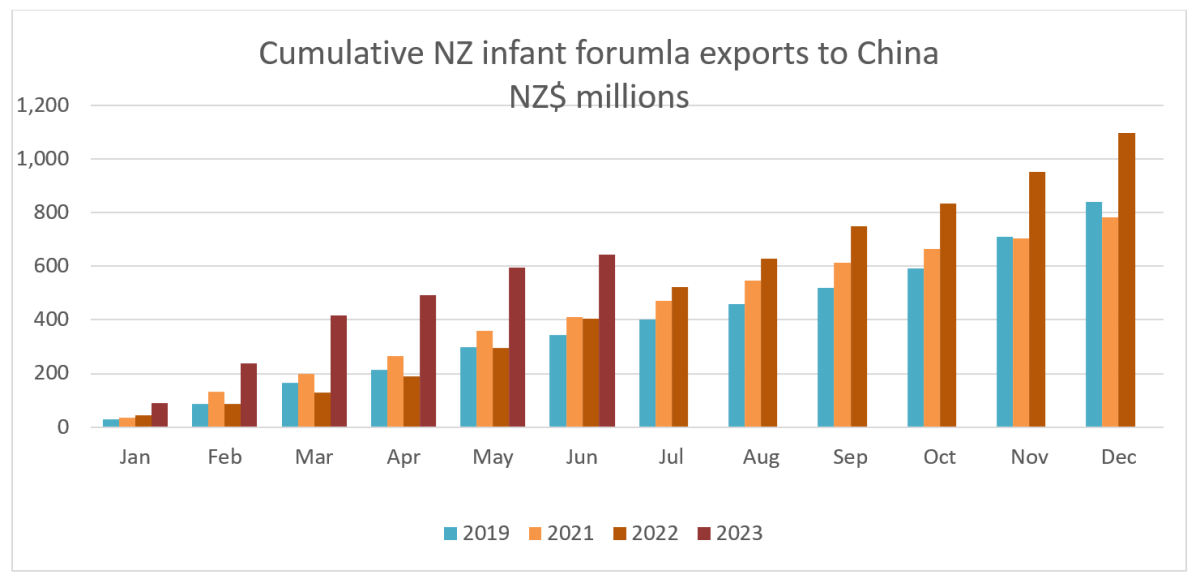

Infant formula export earnings performed strongly in the year ending December 2022, up by 40% yoy and 30% increase from pre-pandemic 2019. The cumulative export value was NZ$1.1 billion in 2022. In the year to June 2023, infant formula saw a 59% increase in exports yoy. This increase is a result of both greater export volumes and an uplift in value. Abbott Laboratories plant closures in the US with food safety concerns and product recalls caused a shock in global infant formula market dynamics. Aotearoa New Zealand manufacturers’ reputation for quality, health and hygiene, has filled some of the gap.

Chinese government regulation around baby food has also tightened. In February 2023, new stricter registration requirements were introduced, requiring all infant formula manufacturers to re-register under these new conditions.

At a macro level, the China infant formula market faces longer term downward pressure. China's declining birth rate is impacting the overall size of the infant formula market, though it remains one of the largest in the world. Imported infant formula continues to fetch a higher price than domestic infant formula, although the price gap is narrowing and domestic brands are now the most consumed.

Meat and meat products

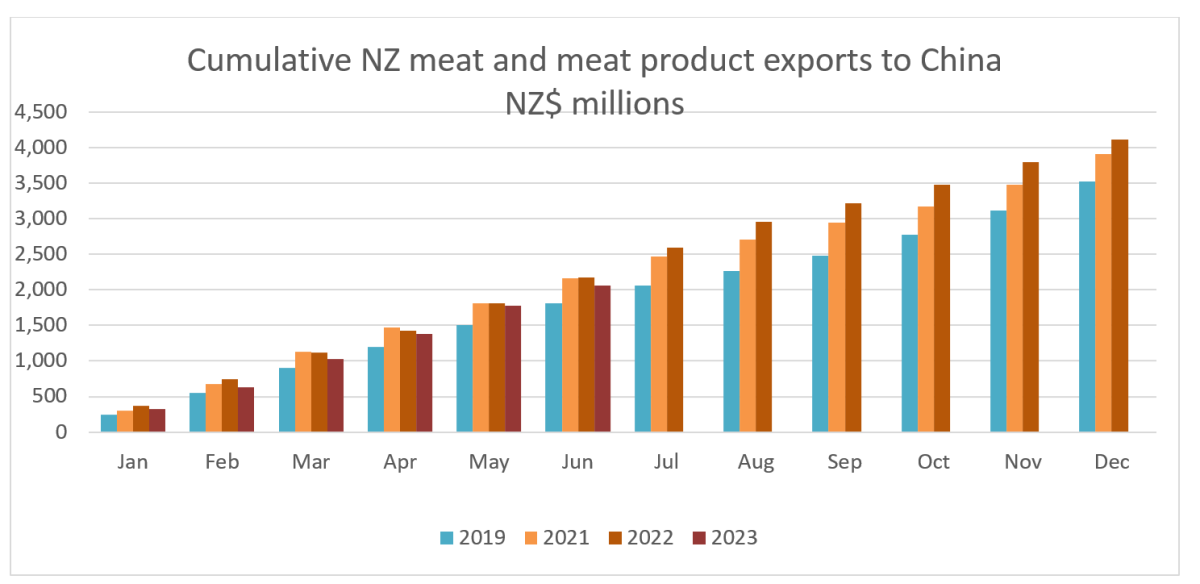

Meat exports to China in the year ending December 2022 grew 5% yoy, with a cumulative export value of NZ$4.1 billion. In the six months ending June 2023, however, export earnings fell 5%. There has been a drop in prices, especially for beef, while volumes remain steady or increased. Brazilian beef has re-entered the market. Despite the mixed result, overall the sector has shown stable growth in China. Over three years, the sector has grown year to year on pre-pandemic (2019) levels.

Forestry

Forestry exports have declined in value in China. In 2022 Aotearoa New Zealand’s forestry product exports to China decreased by 5% on 2021 figures, to NZ$3.6 billion of exports. Export earnings fell again in the year to June, dropping 22% yoy, with global log prices in sharp decline. The weakened demand for forestry products is linked to a slowdown in China’s construction sector. The property sector has less demand for structural timber, interior decoration, boxing timber, and furniture.

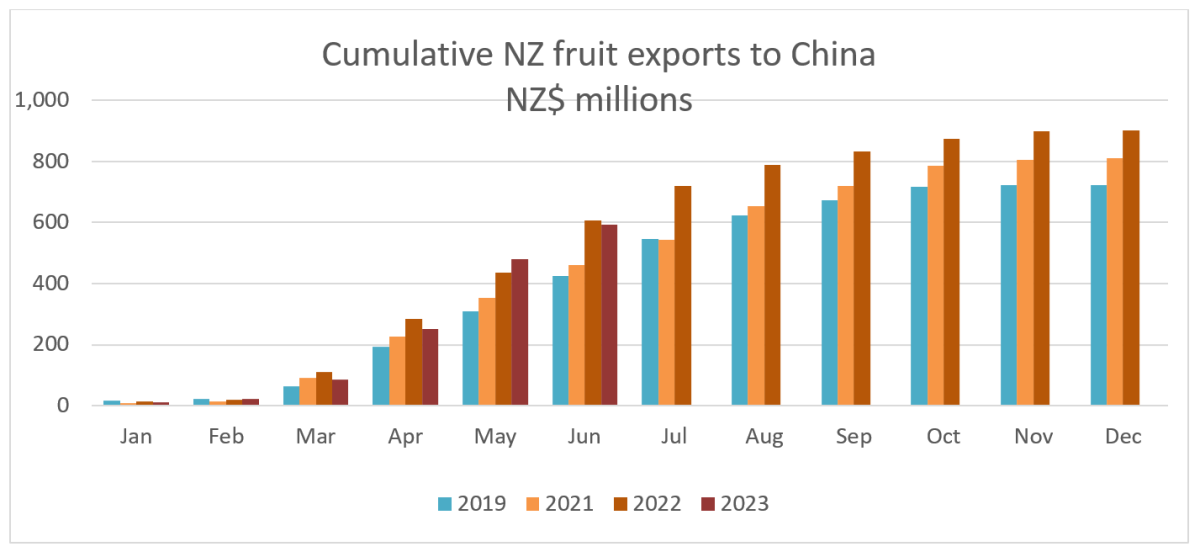

Fruit

Aotearoa New Zealand fruit exports to China reached NZ$901 million in 2022, an 11% increase on 2021 total exports. Fruit exports performed well in 2022 despite COVID-restrictions and generally weak consumer demand. Consumer trust in Aotearoa New Zealand fruit and its health benefits has bolstered demand during the pandemic.

In the first half of 2023 this momentum was largely maintained, with export earnings 2.5% behind 2022 figures. With North Island horticulture regions impacted by adverse weather in the 2022/23 growing season, including Cyclones Hale and Gabrielle, and lower crop volumes – exports and returns may reduce in the second half of 2023.

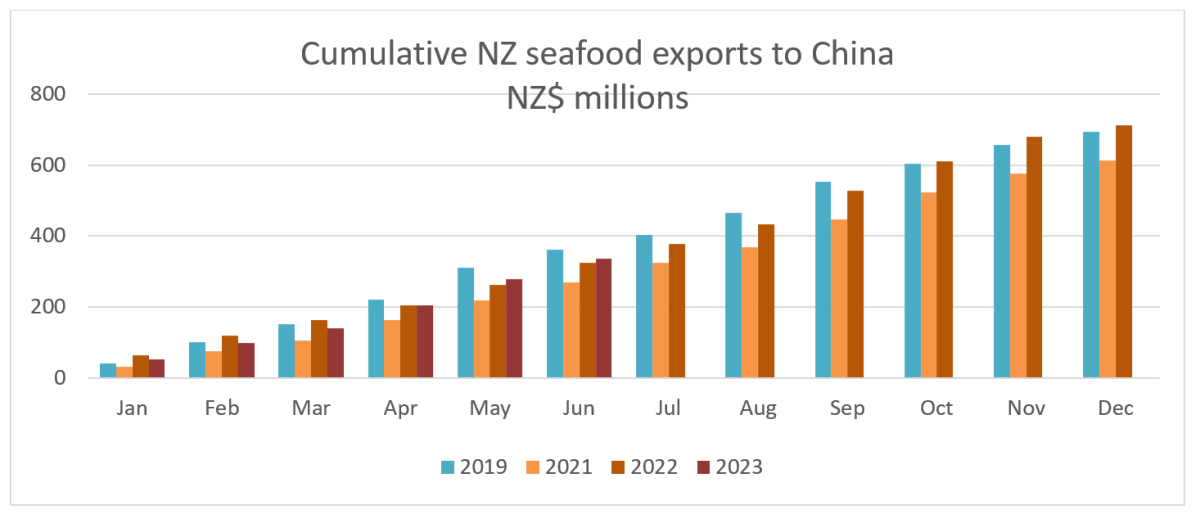

Seafood

Seafood exports to China notched a 16% yoy increase, totalling NZ$712 million for the year ending December 2022. In the first half of the year, seafood exports remained stable, registering a modest 3% increase on the equivalent period last year. Total seafood exports in 2022 were 2% above total seafood exports in 2019, which is a positive indicator for the sector looking ahead.

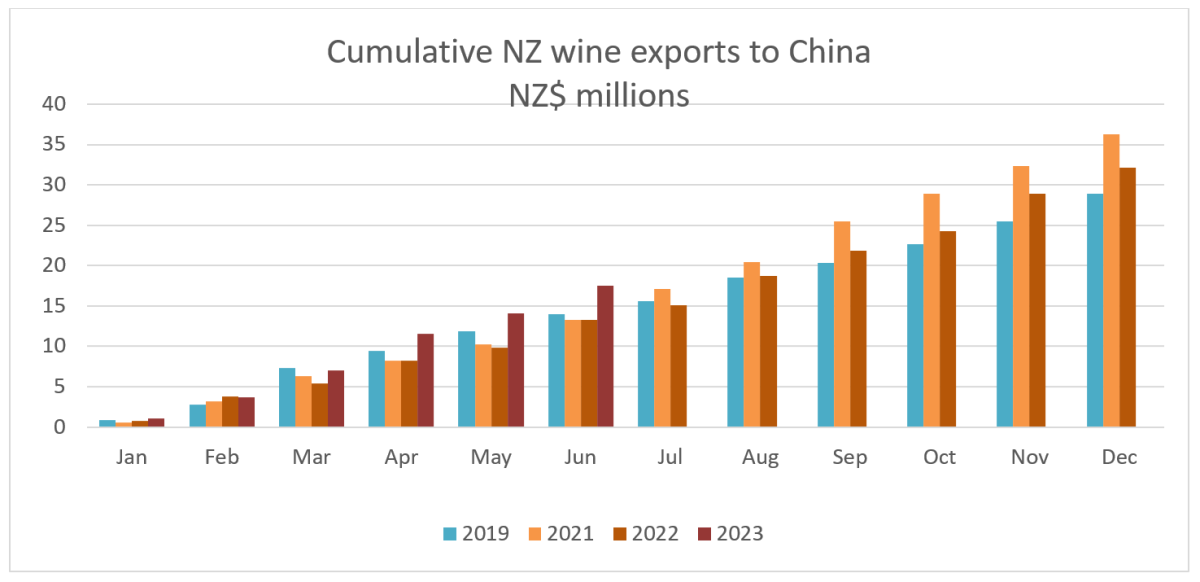

Wine

Aotearoa New Zealand wine exports to China totalled NZ$32 million at year-end December 2022, an 11% yoy decrease. The result still surpassed pre-pandemic levels, up 11% on 2019. Wine exports have performed strongly in the first six months of 2023, up 32% on the equivalent period in 2022. Aotearoa New Zealand per litre returns remain some of the highest of all wine producing countries in China.

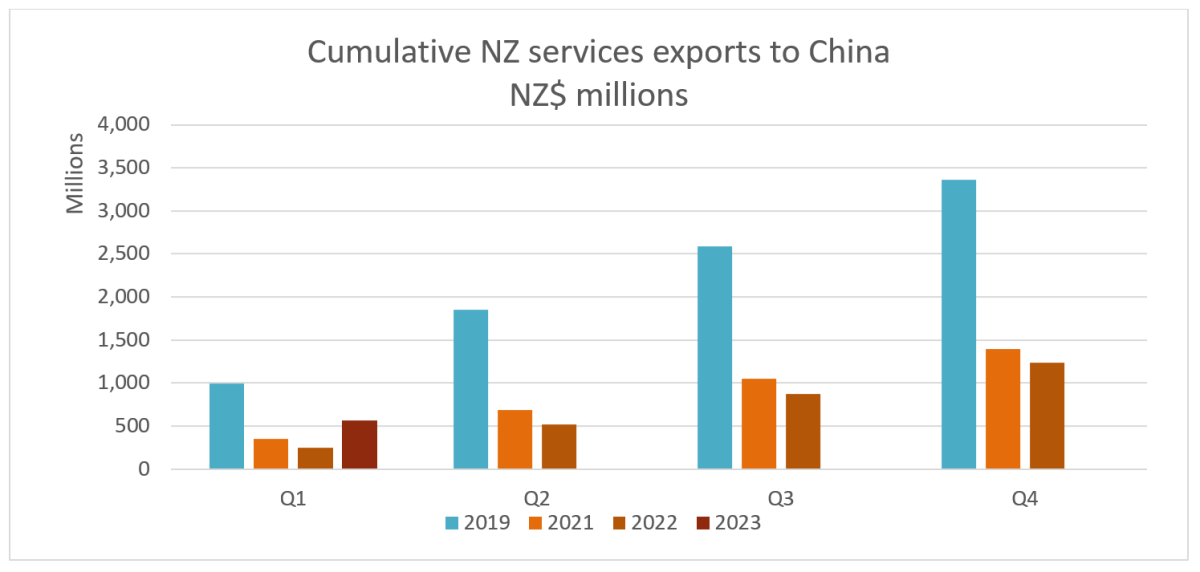

Services

Services trade bore the brunt of disruptions during the COVID-19 period as closed borders limited education and tourism links. This is reflected in the 11% yoy decrease in services exports at year-end December 2022. However Q1 2023 data rebounded 120% yoy, on 2022’s low base. While far below pre-pandemic levels, the turnaround in exports is a positive signal for the services sectors going forward.

Note: Regular China market updates and other useful resources are available on the NZTE website(external link). Exporters can also sign up for myNZTE for China market information on a number of topics. The Ministry for Primary Industries(external link) regularly provides requirements (Overseas Market Access Requirements or OMARs (login required) and Importing Countries Phytosanitary Requirements or ICPRs) and For Your Information (FYI) documents, including for China, with guidance on exporting issues relating to animal products (such as meat, seafood, honey, and dairy), food products, plant products, and wine.

More reports

View full list of market reports(external link)

If you would like to request a topic for reporting please email exports@mfat.net

Sign up for email alerts

To get email alerts when new reports are published, go to our subscription page(external link)

Learn more about exporting to this market

New Zealand Trade & Enterprise’s comprehensive market guides(external link) cover export regulations, business culture, market-entry strategies and more.

Disclaimer

This information released in this report aligns with the provisions of the Official Information Act 1982. The opinions and analysis expressed in this report are the author’s own and do not necessarily reflect the views or official policy position of the New Zealand Government. The Ministry of Foreign Affairs and Trade and the New Zealand Government take no responsibility for the accuracy of this report.