Supply Chains:

Prepared by the Economic Division in Wellington

On this page

Summary

- MFAT’s network of Posts and the Trade Recovery & Resilience Unit have been monitoring global supply chain disruptions and developments since June 2020.

- This report provides an update on global trends, including apparent stabilisation of sea freight, as well as improvements to air connectivity.

- It also canvasses significant regional developments, including changes to COVID management policies in China, industrial action affecting ports and railways in a number of markets, and a new Ukrainian grain initiative that aims to address shortages in Africa.

- To provide feedback or information relevant to this report, please contact exports@mfat.net

Report

Mārunga moana – sea freight

- Global sea freight prices have continued to stabilise over the quarter. The average cost of shipping a 40-foot container across the world’s major shipping lanes was US$2,238 on 1 January 2023, according to Freightos(external link) (an online freight marketplace that regularly publishes industry data). This compares to US$5,286 in early September 2022, and is edging back towards January 2019 rates of US$1,515.

- However, local economist Nathan Penny notes(external link) that New Zealand may be slow to benefit from lower shipping costs. New Zealand is at the end of global supply chains, and faces pressure from high wage costs as well as a relatively weak dollar. This means it could be months before exporters feel the effects of lower global freight prices.

- Delivery times have also improved recently. According to Flexport’s Ocean Timeliness Indicator(external link), the time taken for containers to travel across the Transpacific Eastbound (China to the US) route decreased from 86 days in late September to 69 days in mid-January. Times for the Far East Westbound (China to Europe) route similarly reduced from 96 days in late September to 74 days now. While pre-COVID travel times were under 60 days in early 2019, these changes nevertheless show continued improvement.

- Strikes in the logistics sector have caused periodic delays and disruptions to sea freight. Port workers, truckers and rail workers have called for better pay and employment conditions around the world. Countries affected include South Korea, France and Kenya, with strikes lasting from a few days to weeks.

- International sea freight capacity may increase this year. Container Xchange reports(external link) that new container ships with a combined capacity of 7.1 million twenty-foot equivalent units (TEUs - the industry standard measure for container capacity) are currently on order globally. Most are due to be delivered in 2023 and 2024. With the world’s total capacity being 23 million TEUs in 2019, the new ships could increase supply. But Mainfreight points out(external link) that older ships may be retired as new ones are brought in, so the overall impact on capacity remains to be seen.

Waka rererangi – air freight

- New Zealand’s air connectivity has continued to grow during the quarter. Routes added over the last three months include Auckland to Dallas-Fort Worth (American Airlines), Auckland to Vancouver (Air Canada), and Queenstown to Brisbane and Sydney (Virgin Australia). Each Auckland to Vancouver flight alone carries between 29-36 tonnes of cargo, including New Zealand lamb, tomatoes, salmon, respiratory equipment and live bees. Air New Zealand has also announced that it will resume direct flights between Auckland and Bali(external link) from March 2023.

- The number of passenger flights operating in and out of New Zealand has increased, aligning with the peak summer season. 2,092 flights operated during December – almost double October’s 1,219 flights – offering exporters additional cargo capacity.

- More cargo-only flights have been operating to and from New Zealand to meet seasonal peaks in demand. Air New Zealand operated two extra cargo-only flights to deliver 500 tonnes of cherries and 350 tonnes of fresh seafood to Shanghai and Taipei for the Lunar New Year. China Airlines also operated eight dedicated cargo aircraft between Christchurch and Taipei during January. These flights carried 800,000 kilograms of high-value New Zealand exports to market in the lead-up to the Lunar New Year, including live lobsters, oysters, chilled salmon and fresh cherries.

- High prices and labour shortages persist across the aviation industry, causing disruption to both air cargo and passenger travel. The Loadstar(external link) (an online platform for supply chain news) reports that pressure is particularly acute in Europe due to poor weather conditions and a high rate of sick leave.

Regional updates

Asia

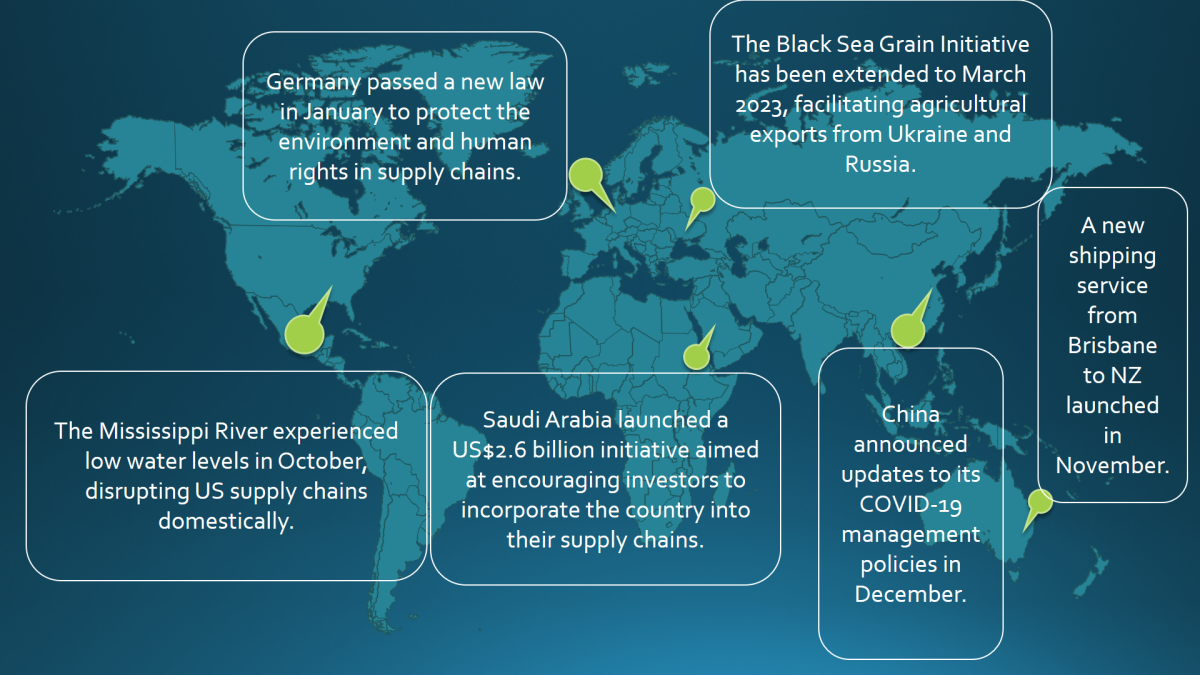

- On 26 December, China’s National Health Commission announced a number of changes to its COVID management policies. While COVID-19 was previously managed under Category A protocols for infectious diseases, it is now being managed under Category B as of 8 January. The relaxed measures mean that quarantine requirements for inbound travellers have been removed, and goods entering China no longer need to be tested for traces of COVID-19. These changes are expected to make it easier to export products from New Zealand to China,

- Air freight capacity to China may increase as airlines consider operating more flights. Air New Zealand reports(external link) an immediate surge in bookings and plans to increase passenger flights between Auckland and Shanghai from three to four per week, beginning on February 4. It also operates two cargo-only services per week on the same route.

- Chinese airports are now open for international passenger transfer connections. This should benefit New Zealand’s global connectivity, as China is an important hub for both passengers and freight travelling between New Zealand and the UK, Europe, India and other parts of North Asia.

Americas

- The US experienced domestic supply chain disruption in October due to low water levels along the Mississippi River. Parts of the river were temporarily closed, which caused queues of more than 3,000 barges. Cargo had to be rerouted to road and rail, which AccuWeather (a weather forecasting company) estimates resulted in approximately $20 million in economic damage. Congestion has now eased due to a combination of rain and efforts by US officials to deepen the river channel by dredging sediment.

- In November, the Federal Drug Administration granted temporary market access for New Zealand’s a2 Milk infant formula in response to the infant formula shortage in the US. For further information about how the New Zealand dairy industry is helping to alleviate supply issues for infant formula, see this market intelligence report(external link) prepared by the New Zealand Embassy in Washington DC.

- The US managed to avoid a railway shutdown that could have caused significant supply chain disruption. US railroads account for about 30% of domestic cargo transport by weight (mostly food, energy, automotive products and construction materials). Unions representing 115,000 rail workers planned a strike for December 9 over pay and working conditions, which could have disrupted domestic supplies of food and fuel as well as exacerbated delays at ports. However, acting in its powers under The Railway Labor Act, Congress passed legislation that adopted an agreement that had previously been tentatively with railway workers’ unions. For further information, see President Biden’s statement on averting a rail shutdown(external link).

Australia

- TS Lines launched a new shipping service between Brisbane and New Zealand in November. This provides access to extra capacity on the route, which Mainfreight characterised in an industry newsletter as a “welcome relief.”

- The Australian Government has appointed(external link) a Strategic Fleet Taskforce to guide the establishment a strategic maritime fleet of Australian-flagged and crewed vessels. The vessels will be privately owned and commercially operated, but also available for requisition by the Government in emergencies.

Europe

- Following strikes between August and October, unions at the Ports of Liverpool and Felixstowe in the United Kingdom accepted pay deals, which will hopefully avoid any delays or disruptions for exporters sending goods to the UK and Europe.

- A new law came into effect in Germany on 1 January aimed at protecting the environment and human rights in supply chains. The Act on Corporate Due Diligence in Supply Chains requires companies with 3,000 or more employees to carry out risk analysis as well as introduce risk management and a complaints mechanism, and report on these measures publicly. The requirements will be extended to companies with 1,000 or more employees in 2024. This may in turn introduce new requirements for suppliers overseas, including in New Zealand.

- In a similar vein, the European Commission is currently considering a draft law to prohibit the sale in the EU market of products made with forced labour. It aims to counter modern slavery across global supply chains. For further information on the European Commission’s proposal, see this market intelligence report(external link) prepared by the New Zealand Embassy in Brussels.

War in Ukraine

- The Black Sea Grain Initiative(external link) signed in July that facilitates agricultural exports from Ukraine through the Black Sea and food and fertiliser exports from Russia has been extended for 120 days through to March 2023 (following a temporary withdrawal of support by Russia on 31 October).

- Ukraine has launched a new initiative called ‘Grain From Ukraine.’ This aims to fund the delivery of 60 vessels carrying Ukrainian grain to Africa and the Middle East by mid-2023, with the goal of alleviating shortages in countries most affected by the food insecurity crisis. Each vessel will cost between US$9-$11 million and carry 25,000 tonnes of grain. Over US$180 million has been raised from more than 30 countries and organisations to facilitate the deliveries.

- The European Bank for Reconstruction and Development has announced(external link) that it will contribute to a US$840 million upgrade of Poland’s deep-water port, DCT Gdansk. DCT Gdansk is the only deep-water port in the Baltic Sea that can receive ultra-large container vessels that move consumer goods and machinery between Europe and Asia. Demand has increased due to the war in Ukraine, and the upgrade will make it one of the top ten biggest ports in Europe. Work is due to be completed in 2025.

Middle East

- Saudi Arabia has announced(external link) the launch of a Global Supply Chain Resilience Initiative. US$2.6 billion is being made available in an effort to turn the country into a global logistics hub.

Supply chain resilience initiatives

- The first in-person negotiating round of the Indo-Pacific Economic Framework for Prosperity (IPEF) took place in Australia in December. Negotiations on the supply chains pillar (one of the four pillars of IPEF) will continue in early February 2023. Canada has expressed interest in joining IPEF, and has separately committed to investing CAD$240.6 million in initiatives targeted at expanding trade, investment and supply chain resilience in the Indo-Pacific region.

More reports

View full list of market reports.

If you would like to request a topic for reporting please email exports@mfat.net

Sign up for email alerts

To get email alerts when new reports are published, go to our subscription page(external link).

Disclaimer

This information released in this report aligns with the provisions of the Official Information Act 1982. The opinions and analysis expressed in this report are the author’s own and do not necessarily reflect the views or official policy position of the New Zealand Government. The Ministry of Foreign Affairs and Trade and the New Zealand Government take no responsibility for the accuracy of this report.