Supply Chains, Primary Products:

On this page

Report

Market overview

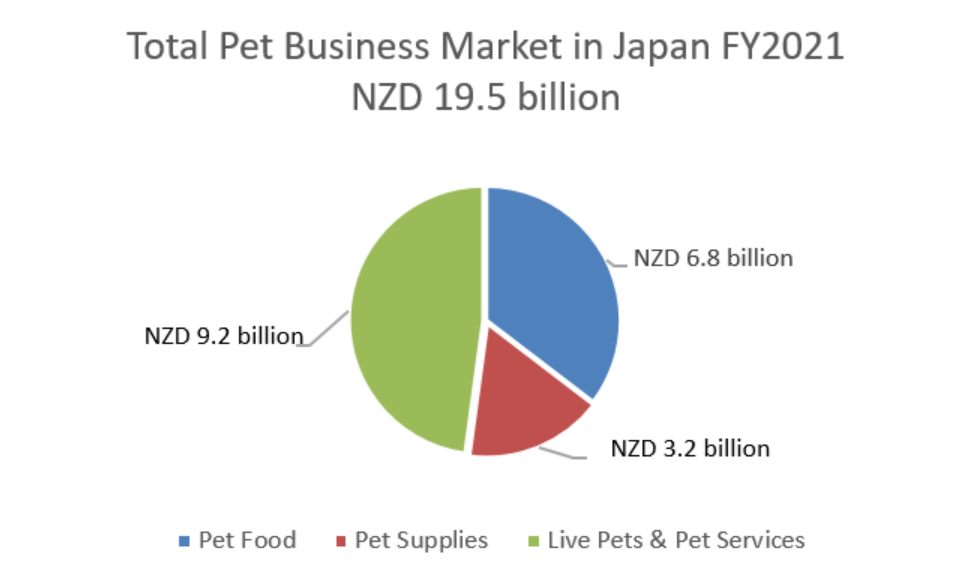

- Pet related market: large and growing. Japan’s pet related market – comprised of 1) pet food, 2) pet goods, 3) live pet sales, medical, and other services – was NZD 19.5 billion in FY2021 (April 2021 – March 2022), up 1.8% year-on-year, and is forecast to increase to NZD 20.8 billion in FY2024.

- Pet food market: expanding. Japan’s pet food market in FY2021 was NZD 6.8 billion, accounting for 35% of total pet related market. It is projected to be worth NZD 8.0 billion in FY2024.

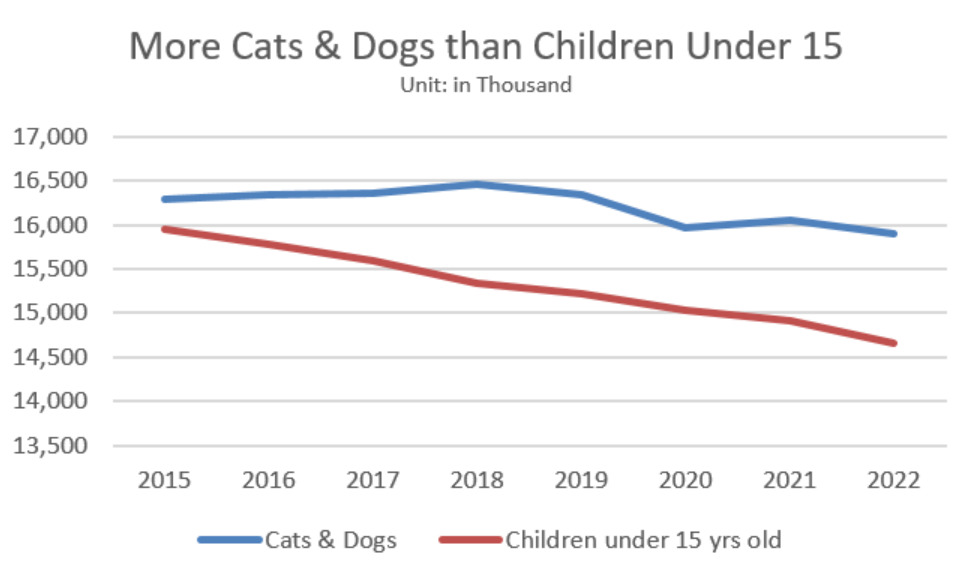

- Number of cats and dogs: more pets than children. There are more cats and dogs in Japan (8.9 million cats + 7.1 million dogs = 15.9 million total) than children aged 15 years and younger (14.7 million). While the number of dogs has decreased gradually over time, the number of cats has remained steady over the last ten years and exceeded the number of dogs since 2017.

- COVID-19 saw an increase of new dog owners. Consistent with global trends, COVID-19 restrictions and self-isolation led to a record number of new dogs being purchased (426,000 in FY2022), the highest in the last ten years. However, with 800,000 to 1 million dogs reaching the end of their life expectancy, the total number of dogs continued its gradual downward trend, despite the increase in new ownership.

- New Zealand’s pet food exports to Japan: small but potential to grow. Japan is New Zealand’s 4th largest pet food export market (following China, United States, and Australia), worth NZD 14 million in CY2022 (up 19% year-on-year). Japan’s imported pet food market is worth NZD 1.1 billion – New Zealand is the 13th largest supplier with a 1.2% market share.

- Positive perceptions of New Zealand pet food in Japan. Japanese consumers and experts view New Zealand pet food as safe and healthy with high standards in terms of ingredients and quality control and falling in the premium and super-premium product categories.

- Crowded market: There may be a risk of saturating the Japanese pet food market given the number of pets has plateaued. The premium/super premium pet food market – that New Zealand companies pioneered in recent years – has begun to attract more entrants from other countries

Pet food

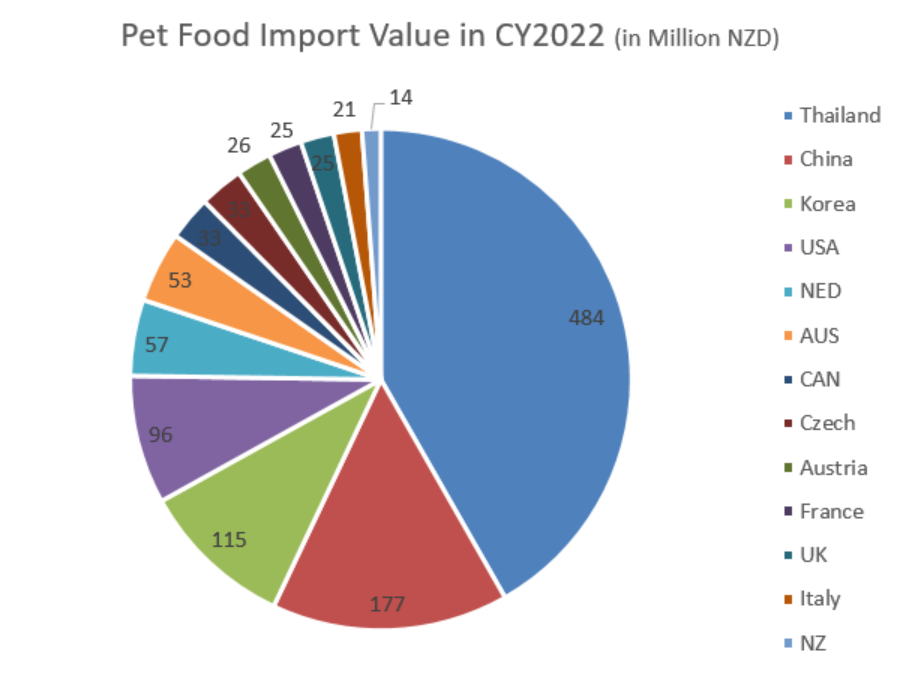

Thailand leads Japan’s pet food imports. Thailand is the largest exporter of pet food to Japan (NZD 484 million, 40% market share in 2022). Thailand was the world’s third largest pet food exporter in 2021 (NZD $2.8 billion, up 27% from 2020). 80% of their exports are private labels for renowned brands across the world such as below.

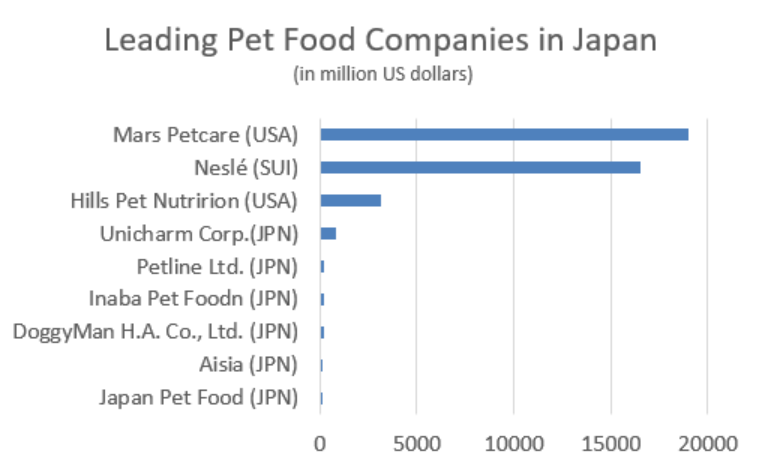

Major pet food players. The Japanese pet food market is dominated by Mars (USA) and Nestle (Switzerland); with Hills Pet Nutrition (USA) and Unicharm (largest Japanese pet food/care company) the third and fourth largest players. Majority of them produce their pet food in Thailand to export to Japan.

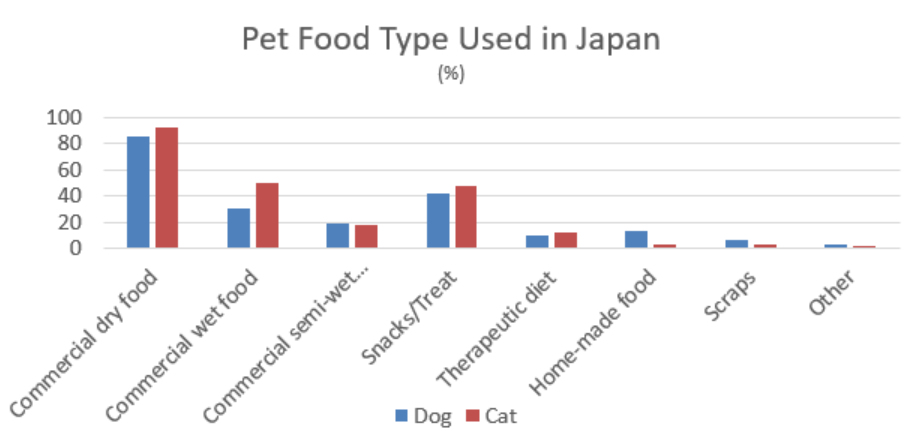

Dry pet food still mainstream. Dry pet food is still prevalent in Japan, with 90% of cat and dog owners buying dry pet food only or dry pet food in combination with wet or semi-wet pet food.

But more people want healthier options. Increasing numbers of “health conscious” pet owners are changing how they see pet food – from “functional animal food” to a “nutritious and tasty meal for a family member”. This has resulted in increasing demand for healthier human grade premium and super-premium pet food, for a high protein and low carbohydrate diet.

Shopping channels, treats/ snacks

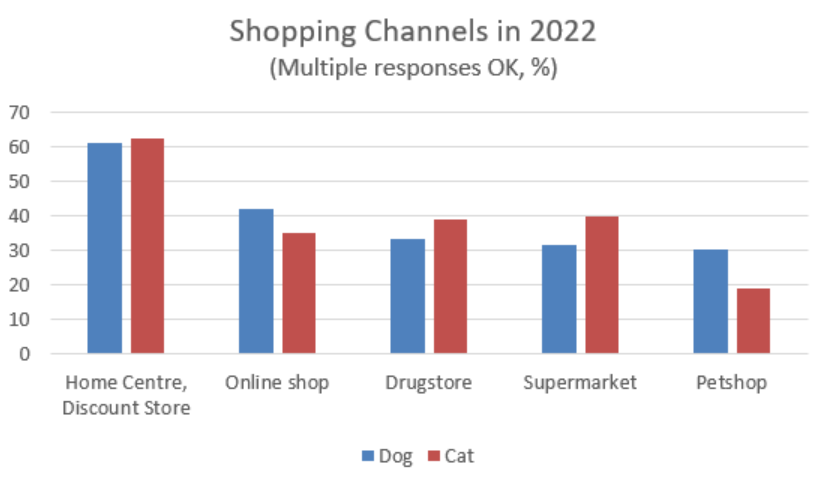

- Shopping channels going online. Home centres and discount stores are the top purchase channel for pet food/supplies, but this is changing with online shops and drugstores becoming more prevalent.

- Fresh pet food trending. New direct-to-consumer (D2C) companies providing fresh pet food are emerging, following trends in the US. Such companies are providing pet owners with healthy raw food and advice from experts on their e-commerce platforms.

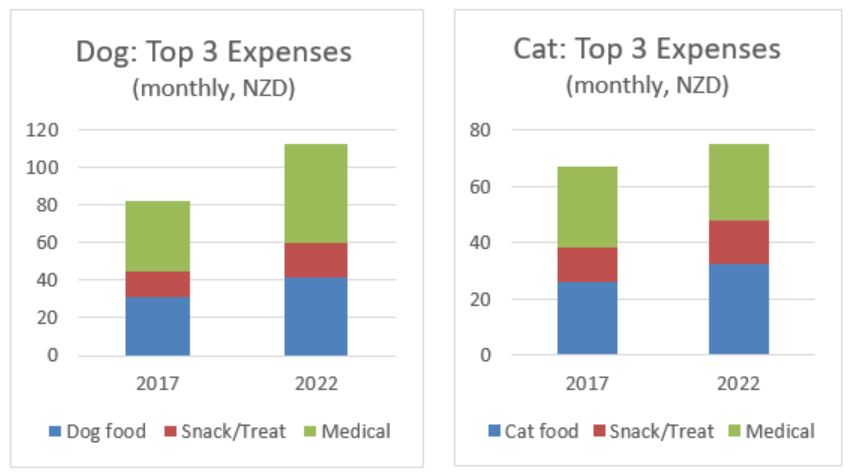

- Majority of expenses: food and medical. For cat and dog owners the top three expenses are: medical treatment, food and snacks/treats – in aggregate accounting for 50% of monthly costs for cats and 37% for dogs.

- Pet snacks/treats expanding: More than 41% of dog owners and 48% of cat owners buy pet snacks/treats, with a market value of NZD 930 million in CY2020 (up 10% from CY2019). The pet snacks/treats market is projected to grow to NZD 1.1 billion by CY2023. This growth in mainly fuelled by the popularity of new products developed by Japanese makers, including health focused functional foods and wet snacks for cats.\

- Spending up on treats/snacks. Spending has increased between CY2017 and CY2022 for dogs (+36%) and cats (+24%) on treats/snacks.

Pet ownership insight

One quarter of Japanese households have pets. Japan has relatively low proportion (27%) of households with pets – compared to 64% in New Zealand.

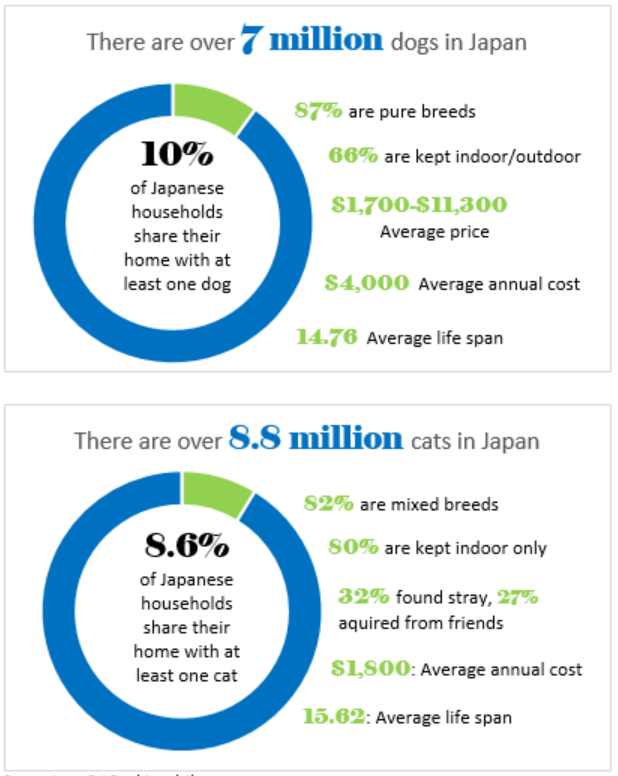

Dogs are the most common. In terms of household ownership – 5.6 million households (10%) have at least one dog. This compares to 34% of households in New Zealand.

Cats are the second most common. In terms of household ownership – 5 million households (8.6%) have at least one cat. This compares to 41% in New Zealand, where cats are the most common pet. (There are more cats than dogs in Japan, but cat owners have 1.8 cats per household, while dog owners have 1.3 dogs per household.)

Dogs have become smaller: Small purebred dogs that are kept indoors are increasingly popular in Japan – the top four breeds are: Toy Poodle (17%), Chihuahua (13%), Shiba-inu (11%) and Miniature Dachshund (8%). This creates opportunities for New Zealand companies exporting targeted functional, premium food and snacks.

Aging pets. Cats and dogs are living longer in Japan. The average life expectancy is 15.6 years for cats (+9% from CY2020), and 14.8 years for dogs (+6% from CY2020). An aging cat and dog population is resulting in more health issues (similar to the aging human population in Japan.)

Super-expensive dogs. 87% of dogs in Japan are purebred – the cost of registered pedigree puppies costs between NZD 1,700 and NZD 11,300. (The average cost of pedigree puppies in New Zealand is NZD 660.) Puppies are bought from pet shops (52%), breeders (16%) and from friends (14%). (In New Zealand, only 10% of puppies are purchased from pet shops.)

Cats less expensive. Cats are more likely to be mixed breeds (82%); adopted from stray (32%); and kept solely indoors (80%). The average cost of cats (NZD 1,800) is less than half of dogs (NZD 4,000).

Market drivers & emerging companies

Trends of pet humanisation

Although the total number of dogs/cats and younger pet owners are flat, the pet market has grown due to “pet humanisation” – Japanese owners increasingly consider their pets to be family members, with whom they spend more time. Due to urbanisation and small apartment living, smaller breeds of dogs and cats have become more popular. “Pet humanisation” has led to the segmentation and diversification of pet products by age, breed, body size, and health / symptomatic care.

Pet owners are willing to spend more money to improve their pets’ quality of life, which has expanded the market for premium and super-premium pet food. Pet food has become a “meal” for one’s “children”, rather than “feed” for “animals”. Owners of small dogs like to dress them in cute designer clothes, and take them for “walks” in custom-made prams.

Area of growth

Dry pet food is still mainstream in Japan – more than 90% of pet owners use dry pet food, alone or with wet food. There is increased demand for natural and organic food – either in dry or wet form – that does not contain artificial ingredients or colouring. Many varieties of “natural pet food” are now available in Japan: air-dried, freeze-dried, wet, semi-wet, as well as “raw food”.

The pet food market in Japan (especially for dog food) has long been dominated by major foreign players – including Nestlé (Switzerland) and Mars (the US) – predominantly selling kibble. Since the 2000s, however, Japanese pet food companies began to develop a new genre of pet treats, and the market began to expand. This trend accelerated rapidly during COVID, which led to owners spending more time with their pets.

Pet snacks are a driver of new growth. For example, pet food manufacturer Inaba Petfood has developed popular products including CIAO Churu (a new paste-type cat snack in a plastic stick), and low-fat chicken retort pouch food for small dogs. Both are “natural snacks” with no artificial colouring or preservatives.

Fresh food: New direct-to-consumer companies

While more than 60 percent of owners buy pet food at the home centre/discount store, an increasing number (42%, +7% compared to five years ago) are buying online. There are some notable new domestic market entrants providing “fresh” pet food via a subscription model with a delivery service. They typically use organic “human grade” ingredients, with the products in individually packed frozen pouches.

While Japan’s economy is the third largest in the world, its pet market is often described as “developing” rather than “mature”, in terms of retail sales volume, number of pets, and consumers’ awareness issues such as pets’ health, ethical treatment of pets, and sustainability of pet products.

This creates opportunities for new direct-to-consumer (D2C) companies providing fresh pet food, challenging the status quo by following trends in the US. These new entrants are aspiring to become “pet wellness” providers, with holistic services to improve pets’ quality of life and online consultation with vets and nutrition experts.

Case study 1: Biophilia Inc. (CoCo Gourmet)

Japan’s leading “fresh pet food” venture company, Biophilia Inc, was established in 2019 by Kota Takahashi, ex-SMBC Nikko Security Intellectual Property specialist turned entrepreneur. The direct-to-consumer (D2C) company makes and sells veterinarian supervised fresh pet food through its e-commerce site “Coco Gourmet”.

Biophilia’s sales have been growing 200% annually, and received a NZD 6.3 million investment from venture capitalists in December 2021. It has a subscription-based system, delivering daily meals for its 84,000 discerning “parents”. It has served over 7 million meals in the last three and a half years.

Case study 2: PETOKOTO (Petokoto Foods)

Another interesting D2C fresh pet food company PETOKOTO Inc, launched in 2008. They have a unique service called “Food Diagnosis” on their e-commerce site, that provides pet owners with customised meals developed by American nutritional veterinary technicians, based on the pet owners’ answers to online questionnaires including breed, age, weight, activity level, and known allergies.

The cost for a three-week supply is approximately NZD 140, 4-5 times more expensive than average in Japan. Since 2008, they have sold more than 5 million servings.

President Taisuke Okubo believes that many pets are overfed, causing them to become obese which leads to illness. Aiming to become a “Pet Wellness Brand”, PETOKOTO also provides “pet life media” that provides information to support owners in caring for their pets.

More reports

View full list of market reports(external link)

If you would like to request a topic for reporting please email exports@mfat.net

Sign up for email alerts

To get email alerts when new reports are published, go to our subscription page(external link)

Learn more about exporting to this market

New Zealand Trade & Enterprise’s comprehensive market guides(external link) cover export regulations, business culture, market-entry strategies and more.

Disclaimer

This information released in this report aligns with the provisions of the Official Information Act 1982. The opinions and analysis expressed in this report are the author’s own and do not necessarily reflect the views or official policy position of the New Zealand Government. The Ministry of Foreign Affairs and Trade and the New Zealand Government take no responsibility for the accuracy of this report.